An Investment Policy Statement (IPS) is the single most important document standing between you and a costly investment mistake.

Your IPS spells out exactly how your money gets invested — your goals, your risk tolerance, your asset allocation… all of it.

And if you work with a financial advisor? Your IPS tells them exactly what they can and can’t do with your portfolio.

In other words: no surprises. No going rogue. No chasing the latest investment fad.

In this guide, I’ll break down what goes into an Investment Policy Statement, why every investor needs one, and how to create yours today.

Key Takeaways

-

An Investment Policy Statement (IPS) outlines your goals, risk tolerance, and investment preferences, giving both you and your advisor a clear roadmap to follow.

-

It helps protect you from emotional or impulsive decisions, especially during market downturns or investment fads, by keeping your strategy grounded.

-

An IPS is essential for both advised and DIY investors, and it should be reviewed regularly to stay aligned with your evolving financial goals.

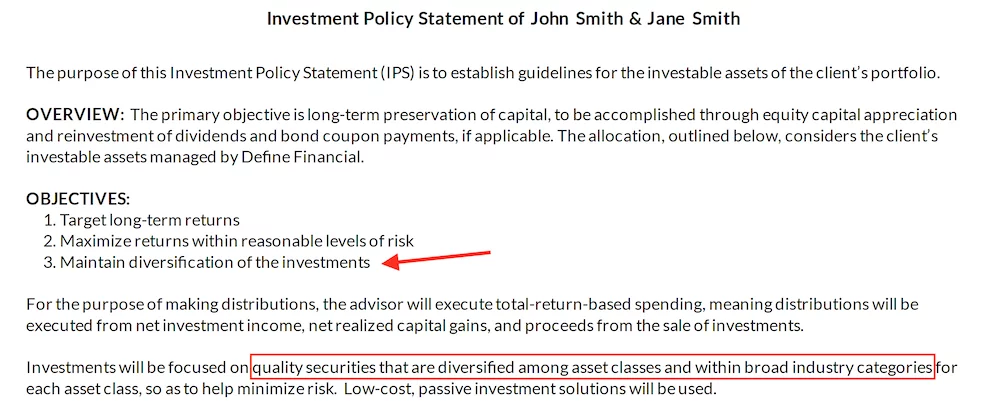

Information Included on an Investment Policy Statement (IPS)

While Investment Policy Statements can look different based on the client, their portfolio, and their investing goals, details found on a simple IPS typically include:

- Your investment objective. Do you want growth, income, or safety?

- Your time horizon. How long do you need your money to be invested?

- Your income needs. Do you want to reinvest and rebalance or take regular withdrawals?

- Your desired asset allocation. How much of your money do you want in each asset class (i.e. stocks, bonds, real estate, cash)?

- Your need for liquidity. How much cash do you need in reserves to fund near-term expenses?

- Your investment philosophy. Do you want your investments actively managed or passively managed? Are there certain asset classes or stocks you would like to stay away from (e.g., tobacco companies)?

Remember, perfect is the enemy of good. Having an IPS is better than not having one at all.

Start simple and know that this is a fluid document that will change over time.

At a minimum, you should review your Investment Policy Statement every year and ask yourself the following questions:

- Have there been any meaningful changes to my investment goals since the IPS was last updated?

- Do I plan to change my asset allocation significantly in the next 12 months?

- Does my current investment portfolio match up with the asset allocation documented in the Investment Policy Statement?

The state of the economy or the stock market should not influence a change to your IPS. Your IPS should only change if your financial needs and goals have changed.

Do Individual Investors Need an Investment Policy Statement (IPS)?

Absolutely! In fact, an IPS might be more important if you’re a do-it-yourself investor.

Here’s why:

DIY investors tend to be more emotionally attached to their investments, which means they’re more likely to panic-sell during a downturn or pile into a hot stock at exactly the wrong time. And that’s expensive.

According to DALBAR’s annual study, the average equity investor has underperformed the S&P 500 by nearly 3% per year over the last 30 years, largely due to emotionally-driven decisions.

A properly written Investment Policy Statement takes the emotion out of it. It gives you a clear set of rules to follow, no matter what the market is doing.

Think back to March 2020. The S&P 500 dropped 34% in just 23 trading days. Investors with an IPS had a plan to follow. Everyone else? Many panic-sold at the bottom and locked in devastating losses.

The takeaway is simple: staying the course with your investment plan is one of the biggest drivers of long-term success. And an IPS is what keeps you on course.

How Can the IPS Help You Better Invest Your Money?

An Investment Policy Statement is most valuable when you’re most tempted to abandon your plan. And that usually happens during two scenarios: market panic and investment fads.

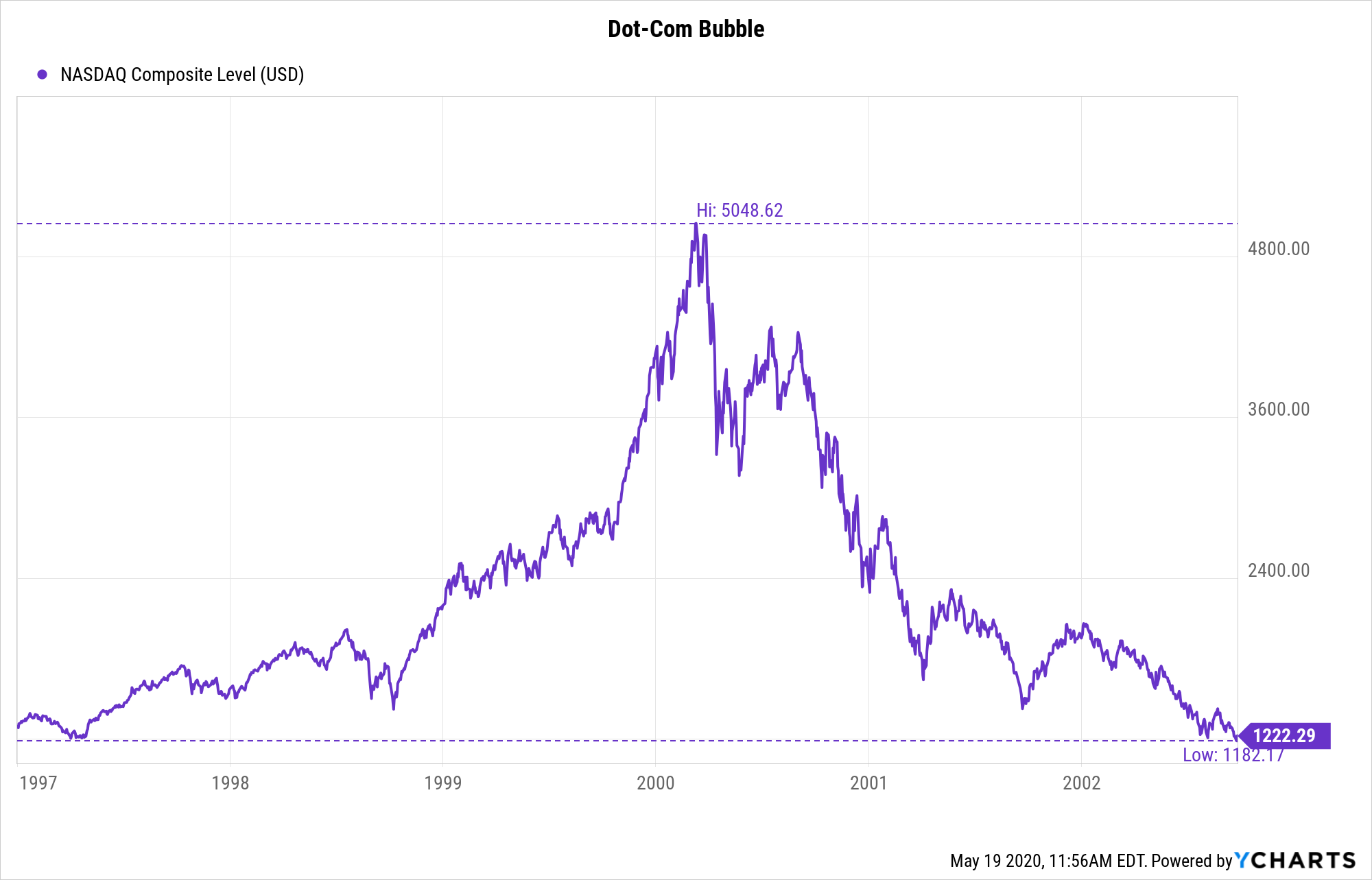

Let’s look at a real-world example. In the late ’90s, internet stocks were skyrocketing. Everyone was piling in. Retirees were moving their entire nest eggs into companies that had never turned a profit.

We all know how that ended.

An investor without an IPS? They had nothing stopping them from going all-in on Pets.com.

An investor with an IPS? Their document would have had clear rules in place — rules requiring diversification across asset classes and prohibiting concentrated bets on a single sector.

Same temptation. Completely different outcome.

That’s the power of an IPS. It’s not just a document, it’s a guardrail that protects you from your worst instincts at the worst possible time.

The Investment Policy Statement (IPS) is Critical to Financial Success

A financial advisor’s job is to help clients reach their stated goals. Maintaining a portfolio that is in line with a client’s unique needs, goals, and risk tolerance does just that.

The Investment Policy Statement (IPS) just takes everything a step further:

It forces investors —and their trusted advisors —to put their investment needs and goals in writing.

If you want to stay the course so you can meet your long-term financial goals, creating an IPS is critical. And remember, this is important whether you work with a financial planner or not.

An IPS will serve as the voice of reason when you’re tempted to invest in risky, currently-trending (read: bubble) investments. If you create this document to rely on its wisdom for the long term, the odds are in your favor that you will achieve your desired financial goals.

Think the IPS has to be complicated? Think again!

- Investment Portfolio Review Checklist (Free PDF)

- Consumers: Download Sample Investment Policy Statement (Printable PDF)

- Institutions & Organizations: Download Sample Investment Policy Statement (Printable PDF)