Choosing the wrong financial advisor can cost you hundreds of thousands of dollars in retirement.

One bad recommendation — the wrong tax strategy, a poorly timed Social Security claim, or an unnecessary annuity — can do irreversible damage to your financial future.

The problem?

There are more than 300,000 financial professionals in the U.S., and there’s no single standard for who gets to call themselves a financial advisor.

That means everyone from a fiduciary CFP® professional to an insurance salesperson can use the same title.

As a CFP® professional with nearly two decades of experience helping people navigate retirement, I’ve seen how difficult it can be to separate trustworthy advice from polished salesmanship.

That’s why this guide walks you through the most important questions to ask a financial advisor before hiring one, the red flags to watch for, and a free printable checklist to bring to your next meeting.

Key Takeaways

- Confirm your advisor is a fiduciary 100% of the time — and get it in writing.

- Ask about total costs, not just the advisory fee. Transaction fees and fund expense ratios can quietly add up to thousands per year.

- If an advisor jumps straight into product recommendations without asking about your life and goals, that’s a red flag.

- Interview at least 3 candidates using the same questions so you can compare apples to apples.

- Your due diligence doesn’t end after hiring. Annual reviews keep your advisor accountable and your plan on track.

- Bring a printable checklist to every advisor interview so you don’t forget critical questions in the moment.

How to Choose a Financial Advisor

With over 300,000 financial professionals in the U.S., knowing how to choose a financial advisor is challenging.

One of the biggest contributors to this challenge is that financial advisors are NOT required to use a consistent title.

For example, you might encounter titles such as: Certified Financial Planner, wealth advisor, investment manager, and financial consultant.

While they might all seem similar, these titles don’t provide insight into what the advisor actually does. Unlike doctors and attorneys, there is no legal standardization of titles and no clear definition for investors to lean on.

In fact, a mortgage broker could call themselves a financial planner!

What to Look for in a Financial Advisor

Before you start interviewing candidates, know what separates a trustworthy advisor from a mediocre one. Here are the most important qualities to look for:

- Fiduciary status — 100% of the time, not just sometimes.

- Relevant credentials — The CFP® designation is the gold standard for comprehensive financial planning.

- Specialization — An advisor who works with clients in your situation (e.g., retirees, high-income professionals) will deliver better advice than a generalist.

- Transparent fee structure — You should be able to understand exactly what you’re paying and how your advisor is compensated.

- A documented planning process — Great advisors follow a repeatable, structured approach to building and maintaining your financial plan.

- A clean regulatory record — Check BrokerCheck and the IAPD website for complaints, infractions, or disciplinary history.

- Strong communication — Look for an advisor who proactively reaches out, responds within 24-48 hours, and communicates in plain language.

Your 3-Step Process For Choosing An Advisor

To help you with this challenge, here are three simple steps explaining how to choose the best financial advisor for your needs:

- Document Your Big Questions and Pain Points. For example, do you want to know when you can retire? How to reduce taxes? Or are you just starting your financial journey and need help establishing a long-term plan?

- Learn About the Different Types of Financial Advisors. Each type of advisor has a different service model and fee structure. Your specific needs and pain points—coupled with your personal preferences—will help you identify the right type of advisor for you.

- Interview and Evaluate 3-5 Financial Advisors. The best financial advisors will display patience during the interview and welcome your hard-hitting questions. They should also provide a detailed process to help you further evaluate them.

Bonus Tip: Before officially hiring a financial advisor, review their professional background for infractions, client complaints, felonies, and more. You can quickly do this at no cost at BrokerCheck and the Investment Advisor Public Disclosure (IAPD) website.

A good advisor will welcome your questions — even the tough ones! If someone gets defensive or evasive during the interview process, consider that your first red flag.

Questions to Ask a Financial Advisor in Your First Meeting

Your first meeting with a financial advisor is essentially a job interview, except you’re the one doing the hiring.

The questions below are organized by category so you can focus on what matters most to your situation. I recommend asking every question on this list, but if you’re short on time, prioritize the first five. They’ll reveal the most about whether an advisor is worth your trust.

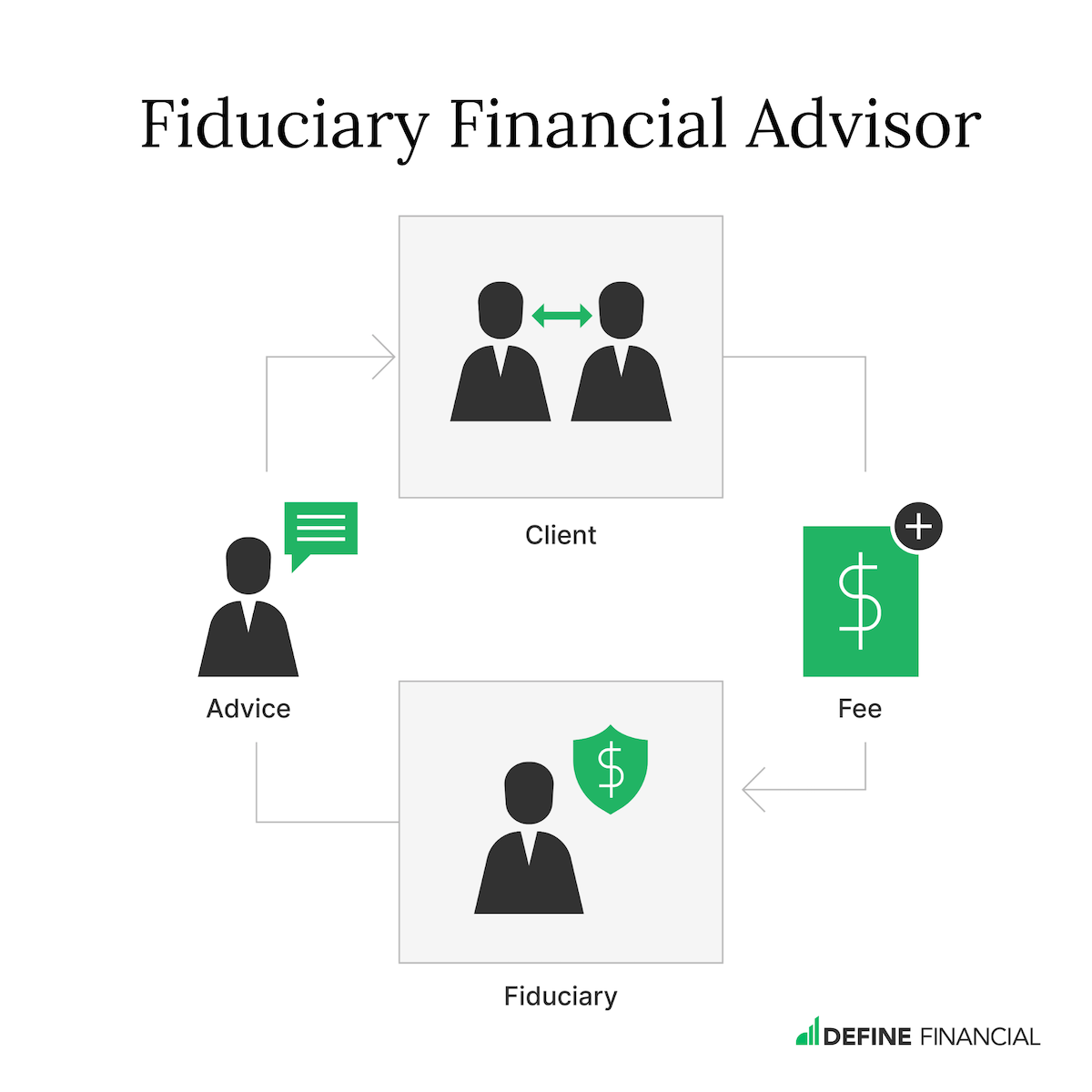

1. Are You a Fiduciary (100% Of the Time)?

A fiduciary financial advisor is legally required to put your interest first. They are also prohibited from selling you a financial product (e.g., annuity, mutual fund) in return for a commission. A fiduciary financial advisor’s compensation must come directly from you (the client) and be a transparent line item on your statement.

If you want your interests to be ahead of anything (and anyone) else, it’s critical to ask an advisor you’re interviewing the following question:

“Are you a fiduciary 100% of the time?”

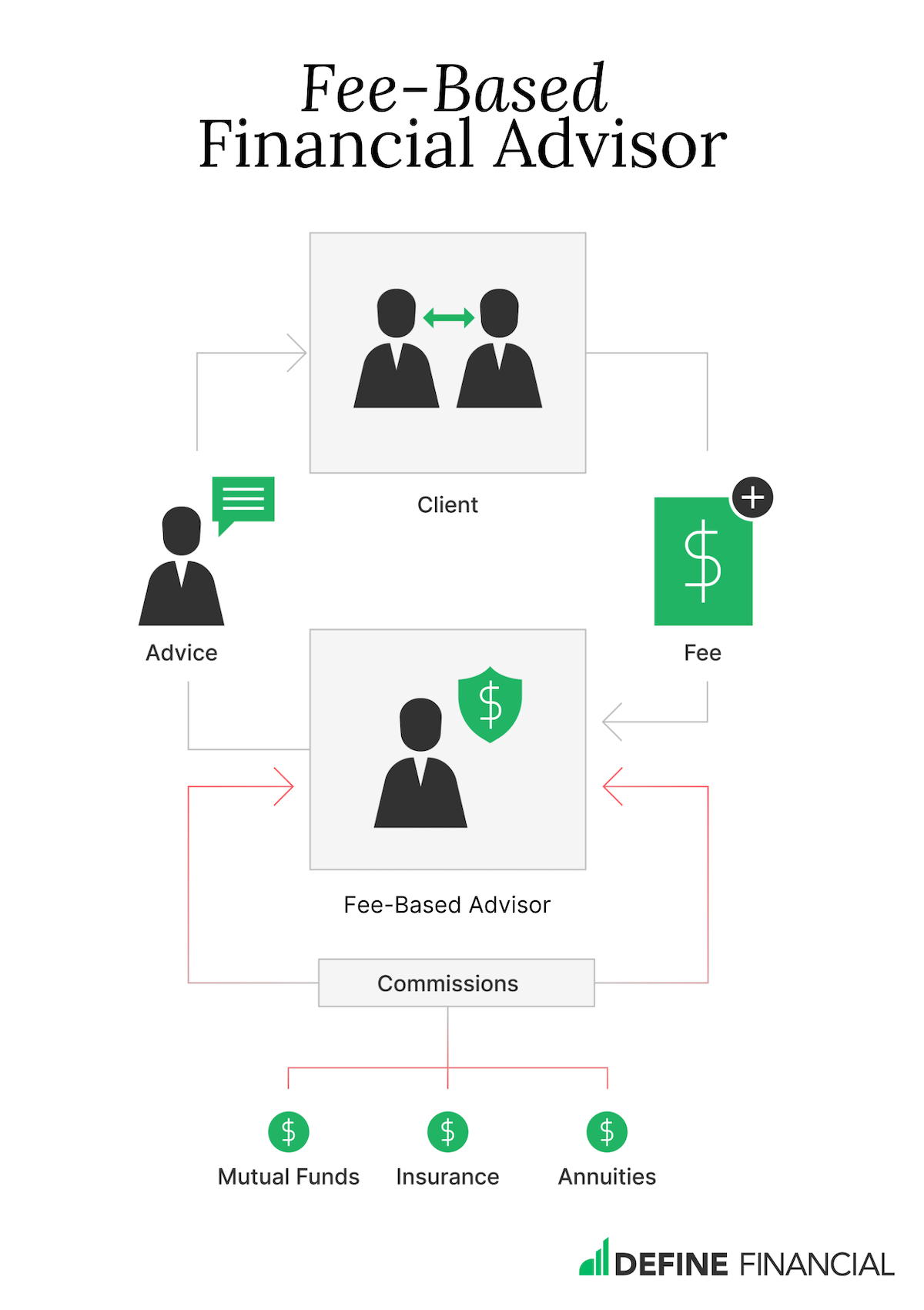

Unfortunately, most of the responses will be, “No!” And that’s because most advisors are “dually registered” (a.k.a. fee-based).

A “dually registered” (a.k.a. fee-based) advisor can take their fiduciary hat on and off. In other words, they are NOT a fiduciary 100% of the time. One day, they are a fiduciary putting your interests first; the next, they sell you an insurance product with hidden fees and commissions.

When a financial advisor acts as a fiduciary 100% of the time, you don’t have to wonder how they are being compensated.

✅ What to listen for: A straight “yes” without qualifiers. If they say “sometimes” or “when applicable,” that’s a red flag. When in doubt, ask them to sign a Fiduciary Statement of Commitment. Download a sample here.

🚩 Red Flag: Any hedging, qualifiers like “when applicable,” or reluctance to put fiduciary status in writing.

2. What is Your Specialty and How Many Clients Do You Serve?

It’s critical to ask advisors what type of clients they specialize in working with. After all, you wouldn’t go to a personal injury attorney if you needed help with a divorce.

Here are examples of financial advisor specializations:

- Specific professions such as doctors, teachers, or Optometrists.

- Employees of a major company, like Broadcom or Microsoft.

- Certain age groups, like millennials or baby boomers.

- Specific life stages, like pre-retirees or recent widows/widowers.

It’s important that the professional you hire has the right expertise to help with your specific situation. It’s also comforting to know they’ve successfully helped other clients with similar needs and challenges.

Speaking of other clients, asking an advisor how many clients they serve is another good question for two reasons:

- It will help indicate how much time they have to spend with you.

- It highlights how personalized (and customized) their services are.

On average, an experienced lead financial advisor can serve about 100 clients. That number can increase or decrease depending on their service model, fee structure, and total team headcount.

✅ What to listen for: A clear, specific answer about their niche — and a client count under 150.

🚩 Red Flag: An advisor who says they work with “everyone” or can’t give you a straight answer on how many clients they serve.

3. What Is Your Experience With Complex Financial Planning?

The number of years a financial advisor has been in business is not the only measure of their experience. The most important factor is the type of experience they have in solving specific problems.

Some examples include:

- Reducing taxes in retirement (e.g., learning how to avoid IRMAA and Navigating the Medicare IRMAA tax brackets)

- Creating tax-efficient retirement income

- Increasing tax deductions through charitable giving (e.g., donor-advised funds)

- Lowering risk while maximizing investment returns

- Optimizing insurance policies in retirement

- Helping you transition into retirement (e.g., writing a retirement letter to your employer)

While you are asking them about their experience, you might also ask:

“Does your firm have a documented process for providing financial planning services and investment advice?”

This process should include how they gather your data, analyze your unique situation, and arrive at their recommendations. It should also include a methodology for implementing and monitoring this advice.

Lastly, one tip for gauging an advisor’s experience level is to ask about professional designations. The most prominent designation is the Certified Financial Planner™ or CFP® certification. A CFP® Professional must adhere to strict ethical standards, complete a series of rigorous coursework and exams, have at least three years of financial advisory experience, and have a four-year college degree, and take continuing education classes each year.

✅ What to listen for: Specific examples of problems they’ve solved for clients like you, plus a documented planning process.

🚩 Red Flag: Vague answers about experience or an inability to describe their planning process.

4. What Is the Total Cost to Work With You?

Just because a financial advisor is a fiduciary 100% of the time does NOT mean it’s easy to understand the all-in costs.

Here are some of the common fees you might pay when working with a fiduciary:

- Advice Fees. These can be billed as hourly fees, one-time project fees, or a percentage of your investments.

- Transaction Fees. These are charged by the custodian (e.g., Fidelity, Schwab) when your advisor buys or sells investments on your behalf.

- Expense Ratio. A mutual fund or exchange-traded fund (ETF) charges this fee to cover operational expenses.

It’s important to note that a fiduciary financial advisor is ONLY compensated by the advice fee. And while they don’t benefit from other fees, they still have a legal responsibility to keep those costs low.

For example, let’s say your fiduciary advisor recommends that you put $100,000 in an S&P 500 fund.

Here are two S&P 500 mutual funds and their expense ratios:

- Rydex S&P 500 (RYSOX) = 1.60% or $1,680 per year

- Fidelity S&P 500 (FXAIX) = 0.015% or $15 per year

That’s a difference of $1,665 per year!

A fiduciary advisor is legally required to recommend the lower-cost option when two investments are identical (like the example above). This is why asking about all the fees you might incur is so important.

Review the advisor’s Form ADV and CRS for a detailed breakdown of their fees and services. These documents are publicly available, and every SEC-registered financial advisor must provide you with copies.

✅ What to listen for: A clear breakdown of all fees — advisory fee, fund expenses, and transaction costs — without being asked to dig.

🚩 Red Flag: An advisor who only quotes their advisory fee and ignores fund expense ratios or transaction costs.

5. What Services Do You Provide?

Asking a financial advisor for a list of their services will help you understand if they:

- Have documented processes and procedures in place to care for their clients properly.

- Focus on one particular area of wealth management (e.g., investment management) or if they take a holistic approach.

Typical services include retirement planning, insurance, investment management, tax planning, and budgeting.

However, highly specialized advisors might offer more nuanced services such as stock option optimization, Roth conversion analysis, Social Security timing, and charitable giving.

An advisor’s list of services should be easy to provide. You might move on to the next candidate if the response is vague or confusing.

✅ What to listen for: A specific, well-organized list of services — ideally available on their website or in a brochure.

🚩 Red Flag: A vague response like “we help with everything” or an inability to articulate their service model.

6. Where Do You (Safely) Hold My Money?

If there is one question to ask a financial advisor that you do NOT want to miss, it’s this one.

Please confirm that your financial advisor uses a reputable third-party custodian to hold your investment/retirement accounts.

Well-known custodians include Fidelity, Schwab, Pershing, and TD Ameritrade.

When your advisor works with a trustworthy third-party custodian, they can’t go rogue with your money. They have limited authority to manage your investments and oversee your accounts.

(Hint hint: Bernie Madoff was NOT using a third-party custodian.)

A reputable third-party custodian also provides investors with FDIC and SIPC insurance. Every third-party custodian provides online access for you to see your accounts. Many also have physical branches across the U.S. for you to visit.

✅ What to listen for: A well-known, independent third-party custodian like Fidelity or Schwab — and the advisor offers you direct login access to your accounts.

🚩 Red Flag: The advisor holds custody of your assets themselves, or they’re evasive about where your money is held.

7. What Is Your Investment Philosophy?

While investments are just one aspect of financial planning, it is critical to ask a financial advisor about their investment philosophy before hiring them.

Do they invest in Exchange-Traded Funds (ETFs), mutual funds, or individual stocks as part of their investment strategy? What about investing in gold? How about hedge funds or alternative investments?

Here are some additional investment philosophy questions to ask:

- How do you incorporate investments in a workplace retirement plan like a 401(k)?

- How many positions do you include in each investment portfolio?

- Can you incorporate individual stock positions that I don’t want to sell?

- Do you have a process for tax-loss harvesting and tax gain harvesting?

- Will you be creating and implementing an Investment Policy Statement (IPS) for me?

In addition to getting answers to these questions, ask for a sample portfolio so you can examine it in detail and see things for yourself. While you’re at it, check those expense ratios!

✅ What to listen for: A clearly articulated philosophy backed by evidence and research — not market timing or “hot picks.”

🚩 Red Flag: An advisor who promises market-beating returns, pushes proprietary products, or can’t explain their approach in plain language.

8. How Often Will We Meet and Communicate?

A good financial advisor should meet with you at least two to four times per year for formal reviews, and be accessible between meetings when questions come up or life throws a curveball.

Before hiring an advisor, get clear answers to these communication questions:

- How often will we have scheduled meetings? Most full-service advisors offer quarterly or semi-annual reviews. Some offer monthly check-ins during major transitions like the first year of retirement.

- How will we communicate between meetings? Ask whether they use phone, email, video calls, or a client portal. Make sure their communication style matches your preferences.

- Who will I actually be working with? At some firms, you’ll meet the lead advisor during the sales process — then get handed off to a junior associate. Ask directly: “Will I be working with you, or someone else on your team?”

- How quickly do you respond to client inquiries? A 24-48 hour response time for non-urgent questions is reasonable. If they can’t commit to that, consider it a yellow flag.

- Do you proactively reach out, or do I need to initiate? The best advisors don’t wait for you to call. They reach out when market conditions change, tax laws shift, or when they spot an opportunity in your plan.

Open, consistent communication is one of the biggest factors in a successful advisor-client relationship. It’s also one of the top reasons people fire their advisor, so ask about it upfront.

✅ What to listen for: A structured meeting schedule, multiple communication channels, and a commitment to proactive outreach.

🚩 Red Flag: An advisor who is vague about meeting frequency or tells you they’ll “be in touch when needed.”

9. What Is Your Plan for Continuity and Succession?

If your financial advisor retires, becomes incapacitated, or leaves the firm, what happens to you and your accounts? This is one of the most overlooked questions, and one of the most important.

Here’s what to ask:

- Do you have a formal succession plan? A documented plan should outline who takes over your account, how the transition works, and how your financial plan continues without disruption.

- Who is your backup? Ideally, there’s a second advisor at the firm who already knows your situation. If the firm is a solo practice with no succession plan, that’s a significant risk.

- What happens to my investments during a transition? Your money should remain at the third-party custodian (e.g., Fidelity, Schwab) regardless of what happens to your advisor. This is another reason question #6—about where your money is held—is so critical.

- Is your firm dependent on one person? Firms with multiple advisors and a team-based service model offer more continuity than a solo practitioner. That doesn’t mean solo advisors are bad, but they need a clear contingency plan.

This question is especially important for retirees. If you’re 65 and hiring an advisor, you may be working with them for 20-30 years. You need confidence that the relationship (and the plan) will outlast any single individual.

✅ What to listen for: A written succession plan, a named backup advisor, and team-based support.

🚩 Red Flag: A solo practitioner with no documented plan for what happens if they can no longer serve you.

10. Can You Show Me a Sample Financial Plan?

Before committing to an advisor, ask to see an example of the work product you’ll actually receive. A sample financial plan reveals more about an advisor’s depth, rigor, and communication style than almost anything they can tell you in a meeting.

Here’s what to look for:

- Is it comprehensive or surface-level? A strong financial plan should cover retirement projections, tax strategies, investment allocation, insurance needs, estate planning, and Social Security timing—not just a portfolio pie chart.

- Is it understandable? The plan should be written in plain language with clear visuals. If the sample plan is 100 pages of jargon and fine print, ask yourself: will I actually use this?

- Does it include actionable recommendations? Look for specific next steps, not just analysis. A great plan tells you exactly what to do, when to do it, and why it matters.

- How often is it updated? A financial plan isn’t a one-time document. Ask how frequently they revisit and revise the plan as your life and the markets change.

- Does it include stress-testing? The best plans model different scenarios: What if the market drops 30% in your first year of retirement? What if inflation is higher than the historical average? What if you experience a catastrophic long-term care event? Stress-testing gives you confidence that your plan holds up under pressure.

Think of the sample plan as a preview of the advisor’s craftsmanship. If they’re proud of their work, they’ll be happy to share it. If they dodge the question, move on.

✅ What to listen for: A comprehensive, clearly written sample plan that covers multiple areas of your financial life — with actionable next steps.

🚩 Red Flag: An advisor who won’t share a sample, or whose sample is a generic one-page portfolio summary.

11. Are There Any Conflicts of Interest I Should Know About?

Even fiduciary advisors can have subtle conflicts of interest. Understanding them upfront helps you evaluate advice with full context.

Here are some conflicts to ask about:

- Does the advisor (or their firm) receive revenue sharing from mutual fund companies or custodians?

- Do they earn referral fees for recommending insurance products, mortgage brokers, or attorneys?

- Does their firm have proprietary investment products they’re encouraged to use?

- Are there any financial incentives tied to recommending certain products or services?

A fiduciary is required to disclose conflicts of interest in their Form ADV Part 2. But not every client reads a 30-page regulatory document — so ask the question directly.

✅ What to listen for: An advisor who openly acknowledges potential conflicts and explains how they mitigate them.

🚩 Red Flag: Defensiveness, dismissiveness, or a claim that they have “zero” conflicts. Every firm has some — the honest ones tell you about them.

Red Flags to Watch for When Hiring a Financial Advisor

Throughout this guide, I’ve highlighted specific red flags for each question.

Here’s a summary of the most serious warning signs I’ve seen in nearly two decades as a CFP® Professional:

- They’re not a fiduciary 100% of the time. If they can sell you products on commission, their incentives may not always align with yours.

- They get defensive when you ask tough questions. A confident, ethical advisor welcomes scrutiny.

- They jump straight to product recommendations. If an advisor starts pitching annuities or insurance before asking about your goals, walk away.

- They guarantee returns. No one can guarantee investment returns. Anyone who claims otherwise is either lying or doesn’t understand markets.

- They pressure you to act quickly. A good advisor gives you time to think, compare options, and make an informed decision.

- They can’t explain their fees clearly. If you can’t understand how they’re compensated after asking, that’s a problem.

- They don’t have a succession plan. If something happens to your advisor and there’s no plan in place, your financial plan could be in jeopardy.

- They hold custody of your assets. Your money should always be held by an independent third-party custodian.

- They have complaints on BrokerCheck. Always check an advisor’s regulatory history before hiring them.

- They don’t ask about your life. The best advisors start with your goals, values, and concerns — not your portfolio balance.

Understanding the Role of a Financial Advisor

It’s crucial to understand what a financial advisor does and the scope of advice they can provide. This knowledge helps align your expectations and influences the questions you might ask during your search.

What Does a Financial Advisor Do?

A financial advisor is a professional who is paid to give financial advice to individuals and businesses.

Their expertise typically includes guiding you through investment strategies, retirement planning, education funding, estate and legacy planning, tax issues, and insurance decisions.

Like a doctor, financial advisors diagnose your current situation and identify and implement strategies to help you reach your financial goals.

Key functions:

- Investment advice

- Retirement planning

- Tax-mitigation strategies

- Education funding

- Insurance and estate planning

Financial advisors can offer one, some, or all of the services noted above. Understanding their role and the services they provide will ensure you hire the right advisor and only pay for the services you need.

Types of Financial Advisors

There are various kinds of financial advisors, each differing in their services, compensation, and interactions with clients. More specifically, I would argue there are five different types of financial advisors:

- Full-Service Financial Advisors: Build and maintain your financial plan, manage your investments in accordance with the plan, and help with all of the different aspects of your financial life. Tax planning, insurance planning, cash flow management, coordination of retirement withdrawals, etc. If there is something they don’t do (or can’t do), they will typically offer to find the right third-party expert to help. In other words, they do all of the heavy lifting for you.

- Investment Managers: Strictly manage your investments for an ongoing fee. They don’t evaluate other aspects of your financial life or provide planning services. They buy and sell investments on your behalf based on the amount of risk you are willing to take. An Investment Manager could be a real-life person or a technology service (e.g., Robo-Advisor) managing your money via algorithms.

- Advice-Only Advisors: Do not manage your investments or implement any of the planning recommendations they make. Advice-only advisors answer your questions and tell you what you need to do in return for a fee; it’s your responsibility to take action and implement everything properly. This arrangement might be akin to a fitness expert creating a custom workout plan for you but not actually joining you at the gym to hold you accountable and ensure you implement the plan correctly, like a personal trainer.

- Insurance Agents: Help you solve a specific insurance need (e.g., Long Term Care Insurance) by educating you on different insurance options, shopping the market, and securing the best policy at the best price. Much like an Investment Manager, Insurance Agents will typically evaluate insurance needs in isolation and refrain from analyzing your entire financial life.

- A La Carte Advisors: Instead of giving advice, they typically take and process orders on behalf of their clients. If you want them to sell XYZ stock and buy ABC stock, they’ll process the trades for you in return for a commission. If you need a business loan, they’ll show you what they have available and help you apply. A la carte advisors are a good fit for people who want to maintain control over their investments and financial plan, but need assistance with execution from time to time.

» Learn more about the 5 Different Types of Financial Advisors

Understanding the type of financial advisor you’re engaging with is important for setting expectations and ensuring your financial needs and goals align with their service and fee structure.

Final Thoughts and Resources

Choosing a financial advisor is one of the most important financial decisions you’ll make, especially as you approach or enter retirement.

The questions in this guide will help you cut through the noise, identify the right type of advisor, and avoid the most common (and costly) mistakes.

Here’s what to remember:

- Ask all questions. Don’t skip the uncomfortable ones. A great advisor will welcome every question on this list.

- Watch for red flags. If anything feels off during the interview, trust your instincts. There are plenty of excellent advisors, you don’t have to settle.

- Take your time. Interview at least 3-5 candidates. This is a long-term relationship that will impact your financial life for decades.

- Verify everything. Review BrokerCheck, Form ADV and CRS, and confirm fiduciary status in writing.

- Bring the checklist. Download our free printable checklist and bring it to every advisor meeting.

In addition to the questions in this article and our checklist, here are a few additional resources to download:

- Questions to ask a CFP® Professional

- Investor Resources and Checklists

- Financial Advisor Interview Questionnaire

Please contact us if you have any questions or would like to evaluate and interview our firm.