What’s the Easiest Way to Save Money?

You may be asking this question if you can’t manage to save money (or if you can’t save as much money as you’d like to). You may think saving money means you need to budget and stick to that budget by diligently tracking every purchase you make. That’s nonsense! I’ve got a super easy way to save money:

Automation!

When it comes to saving money, automation means setting up automatically pulling money from your checking account and putting that money into a savings (or investment) account regularly. With a one-time setup, you’ve committed to consistently save money. Thanks to automation, you can make yourself save money without thinking about it! You just set it and forget it.

You’re Probably Already Saving Money in the Easiest Way Possible

Are you contributing to your employer’s retirement plan (like a 401(k), 403(b) or 457)? If so, then you’re already taking advantage of automated savings! When you use a 401(k), money gets pulled from your paycheck and invested before you have a chance to spend that money! Obviously, automatic paycheck deductions for your company’s retirement plan makes saving money very easy.

And just like if you were to set up automatic transfers to move money from checking to your savings, there is still a one-time set up involved when using a company retirement plan. Can it be a little bit of work and a little bit of a headache? Sure! But doing a little bit of work upfront means setting up yourself for success! And who doesn’t want success!?

What If I Can’t Afford to Save Anything?

Consumer expert Clark Howard suggests starting small. Commit to saving just one percent (1%) – that’s one penny of every dollar earned. One percent is such a small amount of money that you won’t even notice that you’re not spending it. In another six months, bump up your savings rate by another one percent. Keep doing this – increasing your savings rate one percent at a time.

What If I Need Cash for a Down Payment on a Home?

Your 401(k) isn’t the only option for automating investing. You can automate investing for retirement with an Individual Investment Arrangement (IRA) account. Just set up automatic, regular movements of money from your checking account to your IRA account. You can even time these money movements to occur with payday. This way, the moment your paycheck gets put into your checking account, some of that money automatically goes towards meeting your goals.

What’s the Easiest Way to Pay Down Debt?

If you want to aggressively chip away at debt, you can use the same system. Go over and above making the minimum payments on your student debt, your car note, or your mortgage by automating extra payments! You can even use the “start small” strategy: commit to paying just an extra one percent (1%) of your income towards your debt payments. Time these automated payments to occur with your payday. Increase this extra payment by another one percent every six months. Keep doing this until you’ve wiped that debt from your life.

Automation Works for Me

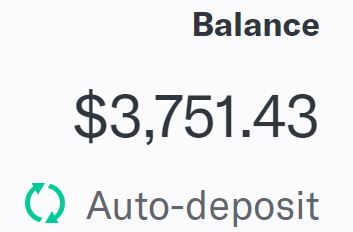

A few years ago, I set up $100 to move from my checking account to an investment account every month. And then I forgot about it entirely. Writing this post just now, I remembered I had this account! So, I took a look. This is what I found:

Here’s what saving $100 every month got me over the course of a few years. I even earned a bit of an investment return!

In short, saving money does not mean having to budget, or be extremely mindful of your spending. To save money, take the easy way out: automate it!