In today’s post, we’re doing a case study on whether whole life insurance is a cost-effective way to invest for your retirement.

Whole life insurance is a type of permanent life insurance where a life insurance policy and investing are combined into one product.

Sounds convenient and easy, right?

Not so fast. We’ll break down the difference between purchasing permanent life insurance versus buying a term life insurance policy and investing the rest.

Key Takeaways

-

Whole life insurance combines investing and insurance, but often comes with high costs, low returns, and hefty commissions.

-

Buying term life and investing the rest (BTID) generally leads to better long-term financial outcomes for most people.

-

Permanent life insurance may only make sense for high-net-worth individuals who’ve maxed out all other tax-advantaged accounts.

Imagine This Scenario…

You’re shopping for a new dishwasher. A salesman approaches you and tells you about a FANTASTIC new product: the dishwashing car!

The dishwashing car comes with a built-in dishwasher! Just think of the possibilities!

You can do your dishes while driving your car!

Now, because this product is so ground-breaking, there are a few catches. This dishwashing car is very expensive (at least compared to buying a car and a dishwasher separately). The maintenance and repairs of this new technology are also very expensive. And lastly, it doesn’t drive very well for a car. It also doesn’t clean dishes very well for a dishwasher.

But, think of the upside:

You can do your dishes while driving your car!

If you think a dishwashing car is a terrible idea, don’t fret. Most people would find the idea ridiculous.

Why? Because there is absolutely no reason to combine a dishwasher and a car. You’re much better off buying the two separately.

What is Permanent Life Insurance?

In the world of finance, there is something quite similar to the dishwashing car. It’s called permanent life insurance.

You get permanent life insurance when you combine life insurance and investing into one product.

There are many, many types of permanent life insurance, including:

- Whole Life

- Universal Life

- Variable Life

- Variable Universal Life (VUL)

- Indexed Universal Life (IUL)

What happens when you buy a permanent life insurance policy instead of simply purchasing your investments and life insurance separately?

Case Study: Permanent Life Insurance vs The Term Life Insurance & Invest Strategy

We’re going to run a little case study in which two strategies are being compared.

The first is purchasing a permanent life insurance policy. The second is buying term life insurance and investing the difference.

For the first scenario, let’s say I use data for a universal life policy from a company called San Diego Life Insurance Company (universal life is a type of permanent life insurance).

Our second strategy is to buy term life insurance and invest the difference (BTID). This is our benchmark strategy. Here, we’ll be buying a regular (inexpensive) term life insurance policy.

Term life is simply a life insurance policy. It works just like your homeowner’s or auto insurance policy. If there is an incident covered by the policy (i.e. a death), the insurance policy will pay out.

Running The Numbers

Our budget for either strategy is the same: $12,000 per year. We’re spending the same amount of money in each case to:

- buy the San Diego Universal Life Policy, or

- buy inexpensive term life insurance and then investing the rest of the money

This post is actually borrowed from an old personal financial planning blog. If you’re interested in getting into the nitty-gritty of the numbers, you can check out the original post. For the cliff notes, read on.

The 20-year difference in a universal life vs. the BTID strategy is approximately $380,000

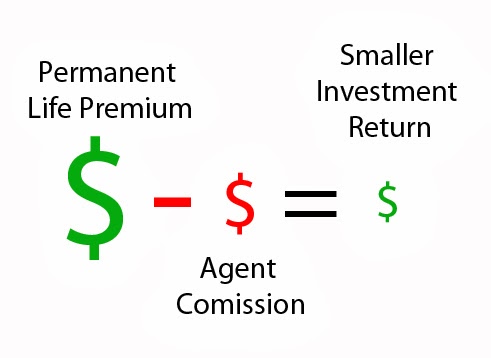

Why the startling difference? In the first year of this universal life policy, there is no cash (surrender) value. Why? Because that money pays for the salesperson’s commissions and insurance company fees. In addition, a cap on the benefits further limits the final value of the universal life insurance policy.

|

| Simple math dictates higher investment returns in the absence of a middleman. |

Conclusion

For certain ultra-high net worth individuals (who have already maxed out every tax-advantaged savings option), a permanent life policy might be the way to go.

However, for most people, the case study above shows that it makes more sense to purchase your investments and your life insurance separately.

Given the data, it is not surprising that many fee-only financial planners advocate for buying a term life policy and then investing separately.

So, the next time a salesperson offers you a life insurance policy that allows you to invest money at the same time – make them a counter-offer. See if you can interest them in a dishwashing car.